The Lowest Hanging Fruit: Getting Rich Slowly

Post updated January 2024.

The single greatest point of leverage for reaching your financial goals is simply understanding how to do it. I’m not asking you to learn new skills, build relationships, or start a business. Though all worthy endeavors, I’m asking you to do something much, much easier. I’m asking you to take advantage of one of the greatest tools accessible to everyone — investing in the stock market. Nothing takes less time and yields greater results. If this is true, why isn’t everyone doing it? Simple.

No one wants to get rich slowly.

- Warren Buffett

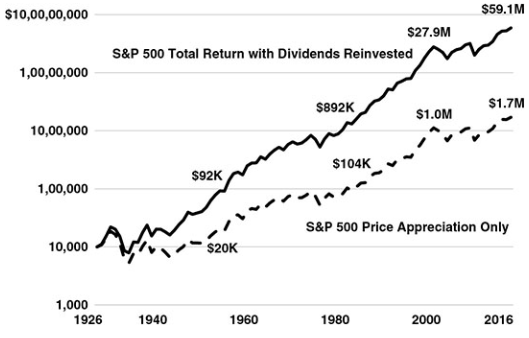

However, getting rich slowly is the easiest way. The stock market is risky, you say? It’s only risky if you are trying to get rich quickly. Year to year it might lose value, but over a long enough time horizon it consistently marches upward. Below shows the performance of $10K invested in the S&P 500 (a basket of the 500 largest companies in the United States, indicative of the market as a whole) starting in 1926. By 2017 the value of that initial investment is $1.7M . And, with dividends reinvested that initial investment grows to $59.1M. The global financial crisis of 2008 is but a blip in the grand scheme of things. True investors, which is what you are, are not concerned with market downturns in the short term because they are long-term thinkers.

Dividends are payments you receive as the shareholder of a company. Remember, when you own stock in a company you are part owner of that company and are therefore entitled to reap its profits. Investing in broad market index funds means you are part owner of companies all over the world (“The Steps” I discuss below will outline how you utilize this investment philosophy). All those executives and employees are working FOR YOU, and you barely have to lift a finger. “Dividends reinvested” means more shares are purchased with the dividends you receive, which then receive dividends themselves. This is the power of compounding interest. It is why time is the single most important fuel that powers the money duplication machine that is the stock market. To illustrate this, if you save only $1K per month from age 25 to 35, assuming a 7% growth rate, you will have almost $1.5M by the time you are 65. However, if you wait until you are 35, and save $1K per month until you are 45, you will only have about $750K by the time you are 65. In each scenario you’ve made the decision to invest the same amount of money, but the time you decide to start doing this (age 25 vs. 35) yields dramatically different results. By starting at age 25, you can make double the money you would if you chose to begin investing at age 35. This is staggering. Time more than anything else is the key to unlocking your financial goals. Let’s get started.

The Steps

These should be treated as a solid starting point and will not apply to everyone perfectly. This is why I am such a proponent of becoming as financially literate as possible. How you save your money is an expression of how you wish to live your life, and no one can make that decision better than you.

The enemy of a good plan is the dream of a perfect plan.

- Carl von Clausewitz

These steps are meant to be done sequentially. Complete each one before moving on to the next. I explain each step in more detail below.

- Save two months worth of expenses in your checking account.

- Pay off high interest debt.

- Save two months worth of expenses in a low-risk, interest bearing account.

- Save two months worth of expenses in an emergency fund.

- If your employer offers a 401k (or 403b) match, contribute enough to take full advantage of the match each paycheck and then contribute as much as you can on top of that.

- Max out your IRA contributions every year.

- Contribute as much as you can to a regular taxable investment account.

The Steps Explained

- Save enough in your checking account so that if all of your sources of income stopped, you could sustain yourself without a change in lifestyle for two months. You never know what will happen, so it’s best to be prepared. This will also give you breathing room to make large purchases without having to dip into savings.

- Paying off high interest debt is a guaranteed return on investment. Paying off a $1K loan with a 20% interest rate is the same as making $200. Since not all debt is created equal (a credit card is going to have a higher interest rate than a mortgage), I recommend reviewing this guide to help you determine how you should pay off your debt.

- Saving two months worth of expenses in a low risk account will offer you greater financial peace of mind and will partially protect you from the cost of inflation. The value of the dollar goes down over time, which is why keeping all of your net worth in cash is actually costing you money. I recommend opening a cash reserve account on Betterment which is very low risk while still earning you interest. Your money in this account is not susceptible to market conditions, which for you means if the market is down you will be able to access your funds if needed with no losses on your initial investment.

- An emergency fund is just that — emergencies only. This is not for spending on vacation, a new car, etc. Ideally you will never need to dip into this account. Treat it as the backstop for your life. I recommend Betterment’s “Safety Net” account, which is made up of 85% bonds and 15% stocks. Bonds are safer and typically earn less than stocks; stocks are riskier and typically earn more than bonds. A portfolio split 85/15 will ensure your money grows, but in a way that offers some protection against market conditions. After accomplishing steps 1 through 4 you have high interest debt paid off and 6 months worth of expenses that are easily accessible. This is an amazing achievement and knowing you have funds to fall back on will give you peace of mind. Now, onto the fun part. Let’s really put your money to work!

- A 401k is a retirement account that may be offered by your employer, allowing you to contribute up to 23k in 2024. Not only are contributions to your 401k not taxed (except for Roth contributions, which you should consider making if you are young and your 401k plan allows it — more on that in the FAQ below), they also grow without being taxed. You will only pay taxes when you begin to withdraw from your 401k account in retirement (more on withdraw restrictions in the FAQ below). If your company will match a percent of your contributions, make sure you at least contribute the maximum percent your employer offers each paycheck. For example, if your employer matches up to 3%, contribute at least 3% of each paycheck to take full advantage of the match. This is free money! On top of just meeting the match, try and contribute as much as you can on top of that. Try and hit the maximum allowable contribution! You will have multiple investment options in your 401k. Be sure to do your research on which fund you choose. This guide is a good place to start (refer to the FAQ below for additional resources).

- An IRA is an Individual Retirement Account which, like a 401k, encourages you to save for retirement by allowing you to deduct your contributions on your taxes unless you make over a certain amount OR your employer offers a retirement plan like a 401k. Also, Roth contributions are not tax deductible - more in the FAQ below. And of course like a 401k, your contributions grow tax-free. An IRA, unlike a 401k, is not something provided by your employer. Anyone can contribute up to $7k in 2024 (if you have earned less than $7k in a year, you can only contribute up to the amount you have earned). Also, if you are a high income earner you might want to consider a Backdoor Roth. This allows you to get around the income limits of a Roth IRA by contributing first to a traditional IRA and then converting it to a Roth IRA. There are tax consequences to this so I strongly consider seeking advisement from a tax professional if you wish to do this. I recommend opening an IRA account on Betterment. Depending on your estimated retirement age, Betterment will recommend an appropriate mix of stocks and bonds. If you are young, it will likely be 90% stocks and 10% bonds, and as you get older Betterment will automatically transition more of your portfolio to bonds to avoid risk.

- At this point you have taken advantage of the two main retirement accounts in the United States, a 401k and an IRA, which allow your investments to grow tax free. Your remaining option is a regular taxable investment account. This account is different from a 401k and an IRA in two important ways. Your contributions will not be tax deductible and the dividends you receive from the stocks and bonds in this account will be taxed. The good news is there are no restrictions on when you can withdraw this money from your account. However, stocks you sell before a year after purchase are taxed at a higher rate than stocks held for longer than year. This is the government encouraging you to invest for the long term. How you invest your money in terms of what percent of your portfolio is made up of stocks versus bonds depends wholly on what you plan to do with the money. Betterment makes it very easy to choose a portfolio that is appropriate. For example, if you are saving for retirement, just like an IRA account, Betterment will recommend a portfolio that is mostly stocks and transitions to a higher percentage of bonds the closer you get to retirement. However, if you are saving up for a major purchase that you plan to make in a year, Betterment would recommend a portfolio made up mostly of bonds because they are less risky over the short term. If you would like to save for a big purchase as well as save more for retirement, simply make two separate taxable accounts. Whatever you do, I highly recommend using Betterment’s Smart Deposit feature that allows you to automatically transfer funds to Betterment when your checking account reaches above a certain amount.

FAQ

What are the key takeaways?

- Not investing your money is actually costing you money.

- Low cost, broad market, index investing is the surest way to reach your financial goals.

- The stock market fluctuates, but over time it marches ever upward.

- Financial literacy gives you control of your life.

- Time is your greatest ally for reaching your financial goals. Start as early as possible. Start right now.

Where can I learn more?

- Google, seriously. This will handle the vast majority of your inquiries.

- The Personal Finance subreddit has several great resources in the sidebar for each stage of your life and is also a great place to ask questions.

- The Personal Finance & Money StackExchange is focused purely on getting your questions answered.

- Mr. Money Mustache (one of my recommended publications) and Mad Fientist are great resources for shifting your perspective on money and reaching financial independence much sooner than you ever thought possible.

- The Little Book of Common Sense Investing (which also makes my recommended books list) will have you convinced that passive index investing (which Betterment utilizes), rather than fancy high cost active investing, is the surest way to reach your financial goals.

How much should I save?

This is a very personal question and really comes down to what your goals are, which is why I encourage you to become as financially literate as possible. Only YOU truly know what your goals are. Having said that, a good general rule is to save 20% of your pre-tax income every year. As for how much you should save based on your age, if you plan on retiring in your 60s a solid rule is your annual salary saved by age 30, twice your salary by 35, three times your salary by age 40, and so on. But don’t fall for the 40 years of work 9 to 5 trap. If you save diligently, and start when you are young, you can easily reach your financials goals while you still have some life in you.

I’m young. Why should I worry about saving now?

Because time is your greatest ally. To illustrate this, if you save only $1K per month from age 25 to 35, assuming a 7% growth rate, you will have almost $1.5M by the time you are 65. However, if you wait until you are 35, and save $1K per month until you are 45, you will only have about $750K by the time you are 65. In each scenario you’ve made the decision to invest the same amount of money, but the time you decide to start doing this (age 25 vs. 35) yields dramatically different results. By starting at age 25, you can make double the money you would if you chose to begin investing at age 35. This is staggering. Time more than anything else is your key to unlocking your financial goals.

How long before I can enjoy the benefits of investing?

On the order of a decade, not several decades. If you save diligently starting in your early 20s, by your mid 30s your investments can can be large enough such that the magic of compounding interest can do the rest of the work. This will allow you to save less and spend more even before you stop working.

Why Betterment and what are some alternatives?

I recommend Betterment because it has low fees, an investment strategy that exposes you to the entire market, is easy to use, and has advanced financial features like Tax Loss Harvesting. Betterment is what is known as a “robo-advisor,” which means a sophisticated computer algorithm, rather than a human, tailors your investment strategy based on your goals. I am a big fan of robo-advisors in general, and there are others like Wealthfront and Wealthsimple that are solid options as well.

If I don’t make a lot of money, can I really reach financial independence/retire early before my 60s?

YES. It all comes down to how much you save, that’s it. Cutting cable TV and your morning Starbucks run can help you retire 8 years earlier. Yes, I’m serious.

It’s not what you make it’s what you have left over.

- Bob T., Legendary Family Friend

I’m having trouble cultivating a saving mindset, what do I do?

First, realize that $100 you spend today is thousands you could have spent in the future had you invested it. Second, understand the simple fact that humans get used to things very quickly. Purchasing a luxury car, designer clothing, and other unnecessary things give you a temporary happiness boost. However, soon that happiness boost becomes the new normal and you are right back where you started– except with less money in your pocket. I’m not telling you to save all your money. I’m telling you to truly think about how you spend it. I’m telling you to spend money on the right things when you are young and save the rest for when you are old.

What is the magical 4% rule?

This refers to the maximum amount you can withdraw from your investments while still sustaining you for your entire life. If you can survive off $25K per year, you only need to save $625K to reach your financial goals and retire. Estimate the amount you need per year to live a comfortable life, multiple this by 25, and that is your goal. This is backed by hard data and even takes into account having to withdraw when the market is down

The market crashed. What do I do!?

Stick to your investing strategy. Absolutely nothing changes. You are investing for the long term, so market downturns in the interim are pointless to worry about. Refer to the chart at the top of this post.

The market is hot right now. Why shouldn’t I wait for a crash to buy in cheap?

It’s always possible a crash is on the horizon, but it’s also possible the market goes up another 20% then crashes only 10%. The reality is no one can predict this consistently, not even professionals. Time in the market is always better than timing the market. Keeping your money in cash while waiting for a crash instead of invested in the market will make you lose out not only gains in the market, but also those precious dividends. Timing the market is extremely difficult to do. Even professionals can’t do it consistently and they do this for a living.

I just read an article about the hottest stocks/funds. Why shouldn’t I purchase them?

Because what is hot today will likely be cold tomorrow. As John Bogle says, “Don’t look for the needle in the haystack. Just buy the haystack!” Investing in low fee broad market index funds (which Betterment does) is the only way to ensure you earn your fair share of stock market returns. Buying and selling individual stocks will cost you trading fees, higher taxes, and more energy. Not even the best Wall Street traders can consistently beat the market over the long run. Warren Buffet, the most legendary investor alive, famously won a $1M bet that the S&P 500 index would beat a basket of hedge funds over a ten year period starting in 2007. Buffet has also gone on record saying that he wants 90% of his fortune to be invested in an S&P 500 index fund.

What other services do you recommend?

I recommend Personal Capital for tracking all your accounts in one place and Credit Karma for building a solid credit score.

How often should I check my investments?

No more than once a month. True investors, which is what you are, are not concerned with market downturns in the short term because they are long-term thinkers.

What are Roth contributions and should I make them?

“Roth” means that your money is taxed before you put it into your 401k or IRA. That means when you withdraw the money in retirement you will not pay any taxes on it. As of 2024, if you make over $146K the amount you can contribute to a Roth IRA begins to diminish until $1161K where you are restricted from contributing at all (no such restriction exists on a traditional IRA). The general rule is you should make Roth contributions while you are young because your salary is likely the lowest it will ever be. However, the reality is no one has any idea what the tax code will be several decades from now when you withdraw from your retirement accounts, so I recommend a split of Roth and traditional contributions.

When can I withdraw from my 401k and IRA?

When you turn 59 ½, though a 401k and an IRA each allow you to withdraw before that under special circumstances. If you withdraw early without a special circumstance, you will pay a hefty fee. A Roth IRA offers more flexibility, and even allows you to withdraw contributions (not money earned on the contributions) without any penalty. Avoid withdrawing early at all costs because keeping your money working for you as long as possible is the surest way to reach your financial goals.

What happens to my 401k when I leave my employer?

You have several options, but likely you will want to (1) keep it where it is, (2) roll it into the 401k plan of your new employer, or (3) roll it into an IRA. Roll it into your new 401k plan if it offers lower fees and better investment options. Note that there are some drawbacks to rolling a 401k into an IRA, including funds in your IRA being less protected in the case of a lawsuit or bankruptcy.

Do I really need a six month buffer?

Everyone has different goals and risk tolerances, which is why I encourage everyone to become as financially literate as possible. Having less of a financial buffer will allow you to invest more of your money and earn more long term, but it offers less flexibility in the short term. The balance is up to you.

What about a dedicated financial advisor?

In a world where investing is a commodity and the internet provides information for free, most people don’t have a complex enough financial situation to justify an advisor. Don’t outsource your financial decision making. Take control of it yourself because it has never been easier. For those that insist, Betterment does offer dedicated financial advisors for a higher fee.

This all sounds great, but ultimately money doesn’t buy happiness so why bother focusing on it?

Don’t make the mistake of thinking money isn’t important. Money is power. It allows you to meet basic needs, support your family, start a business, donate to nonprofits, travel the world, fund your passion, and retire early. Money is what you make of it.

Money is a great servant but a poor master.

- Francis Bacon